What to Do When You Get Dropped: Navigating Florida Home Insurance Non-Renewals

What to Do When You Get Dropped: Navigating Florida Home Insurance Non-Renewals

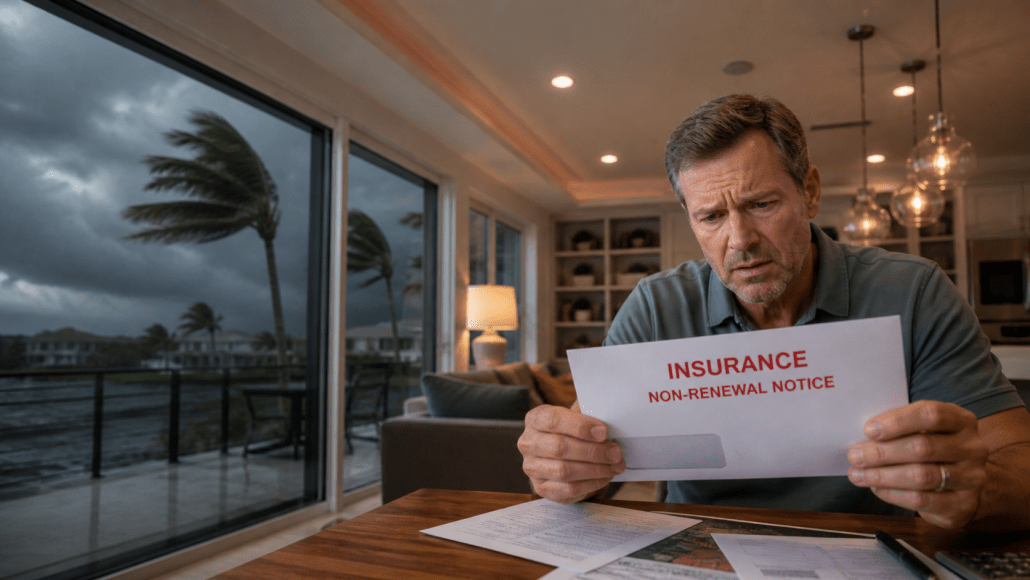

Opening your mail to find a notice of non-renewal from your home insurance carrier is a terrifying experience. In the current Florida insurance market, it is also incredibly common. You are suddenly given a tight 45- to 120-day window to secure a new policy before your mortgage lender steps in and force-places expensive, highly restrictive coverage on your property.

As a Florida-native family agency based in Clearwater, FL, Single Source Insurance intimately understands this crisis. We specialize in stepping in when national carriers step out, helping homeowners across the state secure stable, affordable coverage rapidly.

Immediate Steps: Dropped Homeowners Insurance Florida

If your policy was cancelled or non-renewed, the clock is ticking. Taking the right steps immediately will save you thousands of dollars and protect your mortgage.

- Step 1: Do Not Let Coverage Lapse. A lapse in coverage automatically makes you vastly more expensive to insure in the future.

- Step 2: Read the Reason. Is the non-renewal due to roof age, a recent claim, or simply the carrier reducing their exposure in your ZIP code?

- Step 3: Call an Independent Broker. Captive agents (agents who work for only one company) cannot help you if their company says no. An independent broker has access to dozens of carriers still writing policies in Florida.

Why Are Insurance Companies Leaving Florida?

If you received a Florida home insurance non-renewal notice, you are likely not to blame. Over the last several years, major national carriers have reduced their footprint in the state or pulled out entirely.

This is driven by three primary variables:

- Concentrated Hurricane Risk: Back-to-back active storm seasons have depleted carrier reserves.

- The Roof Age Crisis: Carriers are heavily penalizing roofs over 15 years old. Even if your roof isn’t leaking, the algorithmic risk data forces them to drop the policy to limit liability.

- Litigation Costs: Florida historically accounts for a massive percentage of all U.S. homeowners insurance lawsuits, driving the cost of doing business artificially high.

Because we are Florida natives, we don’t just see you as a risk profile. We know exactly which carriers are actively writing in your specific neighborhood and how to navigate the strict underwriting rules.

Are There Citizens Property Insurance Alternatives?

When homeowners get dropped, many assume their only remaining option is Citizens Property Insurance Corporation—the state-backed “insurer of last resort.”

While Citizens provides vital protection, it should not be your mandated first choice. Citizens policies come with strict coverage caps, and the state legally requires policyholders to jump to private carriers if a competitive rate is offered (known as depopulation).

Single Source Insurance specializes in finding reliable Citizens Property Insurance alternatives. Because we operate out of Clearwater and serve the entire state, our network of private Florida-admitted carriers is robust. We actively shop your property’s specific wind mitigation features and structural updates against our private market network to keep you out of the state-run pool whenever safely possible.

Secure Your Home with Single Source Insurance

Do not face the Florida insurance crisis alone. You should not have to settle for a national call center representative who does not intuitively understand the difference between a hip roof and a gable roof and how that impacts your premium.

If you are dealing with a non-renewal or dropped coverage, you need aggressive, local representation.

Protect your Florida home. Contact Single Source Insurance today. Our family will leverage our deep local network to find the coverage you need to satisfy your lender and protect your greatest asset.

FAQs

1. What happens if my homeowners insurance is dropped in Florida?

If your homeowners insurance is dropped, you typically have 45 to 120 days to secure a new policy before your current coverage expires. If you fail to replace it, your mortgage lender may apply force-placed insurance, which is significantly more expensive and offers limited protection.

2. Can I still get homeowners insurance in Florida after being dropped?

Yes, homeowners can still get coverage after being dropped, but options may be more limited. Independent insurance brokers can access multiple carriers, including smaller regional companies that are still actively writing policies in Florida, increasing your chances of approval.

3. How does roof age affect homeowners insurance in Florida?

Roof age is one of the most important factors in Florida underwriting. Many insurers restrict or deny coverage for roofs over 15–20 years old, regardless of condition. Replacing or certifying your roof can improve eligibility and help secure better insurance rates.

4. How long does it take to get a new homeowners insurance policy in Florida?

In many cases, a new homeowners insurance policy can be approved within a few days to a couple of weeks, depending on inspections, underwriting requirements, and property condition. Working with an experienced broker can significantly speed up the process.

5. What is force-placed insurance and why should I avoid it?

Force-placed insurance is coverage your mortgage lender purchases on your behalf if your policy lapses. It is typically much more expensive and only protects the lender’s interest, not your personal property or liability, making it a costly last-resort option.